Common structures for seller notes

By Mainshares

Nov 1, 2023

In Buying a Business

A common source of financing for small business acquisition is seller financing (sometimes referred to as a seller’s note). Seller’s financing allows the seller to lend the buyer a portion of the purchase price.

There are many reasons why an entrepreneur would pursue seller financing. Seller financing allows an alignment of incentives between the buyer and seller. In essence, the seller provides financing to the buyer because they want to see the buyer succeed. Moreover, better terms are possible through seller financing because seller’s are not constrained by the rules and regulations of the banking industry. Lastly, if there are financing issues with the Small Business Administration (SBA) then the buyer can pursue seller financing.

Common Structures in Seller Financing:

Seller financing can be a bit more customizable than a conventional bank loan; however, there are a few common structures (straight payment, interest only (IO), stand-by, and bullet payments) for selling financing.

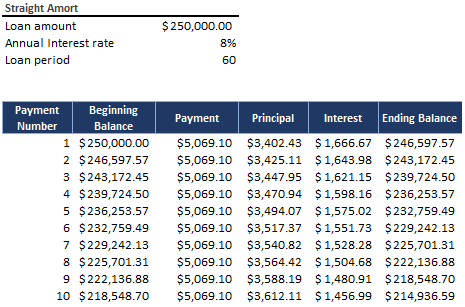

Straight Amortization

For straight payment, this is the most common financing structure. For example, the majority of mortgages and their subsequent payments are calculated on a straight payment basis. These payments include principal and interest. Therefore, as the loan balance is paid down, the payments begin to pay down more of the principal on the loan. Below is an example of straight-line payments:

As noted above, the buyer’s payment is $5,069.10 for every single payment and the proportion of principal that is included in the payment increases with every payment.

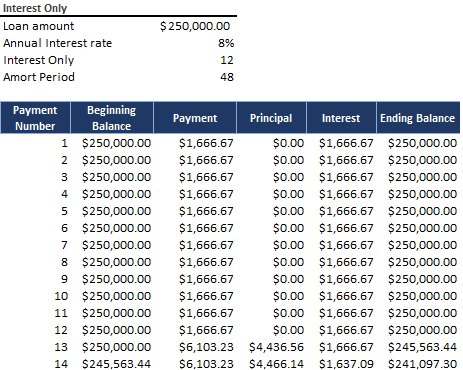

Interest-Only Period

Another common structure is an interest-only loan. These loans are common when a buyer will incur large expenses in the first year or the first couple of years. The goal of the loan is to allow the buyer time to invest in the business and gain control of the business before servicing debt. From a personal loan perspective, interest-only loans are common in construction (e.g., residential construction) because it allows the borrower time to construct the building before making large monthly payments. Below is an example of an interest-only loan:

As is evident from the example above, the interest-only portion of the loan is for the first year of the loan and once the 13th payment hits, the loan acts as a straight payment financing structure. Comparing the two examples, the interest-only loan frees up cash in the first year compared to a loan with straight payments; however, after the first year, the monthly payments are significantly higher than a straight payment loan.

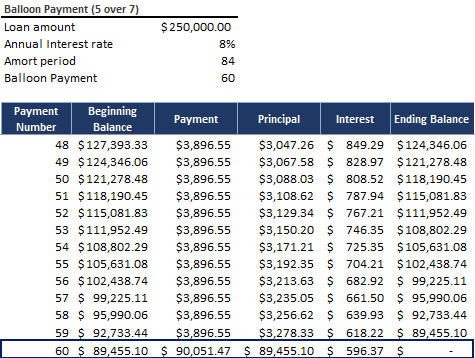

Balloon Payment

A buyer may prefer to have a balloon (or, bullet) payment. A bullet structure is common for buyer’s who plan to refinance to SBA loans or conventional loans. In addition, the buyer may need a few years to accumulate cash before making large debt payments. Common structures within bullet payments are 5/10 (i.e., 5 year loan on a 10-year amort) or 3/5 (i.e.,3 year term on a 5-year amort). There is no preference as to which bullet payment structure a buyer uses. Often, if there is heavy capital expenditures or the business is producing a loss, then a buyer may prefer a 5/10 bullet payment structure. Below is an example of a bullet payment:

In the above example, the bullet payment is structured as a 5/7 (i.e., a 5-year loan with 7-year amortization schedule) loan. As is evident, the payments are significantly lower than an interest-only or straight payment loan; however, the last payment in a bullet payment structure is significantly larger. Typically, what a buyer will do is then refinance the bullet payment into another loan, be that as a bullet payment, interest-only, standby or some other loan structure.

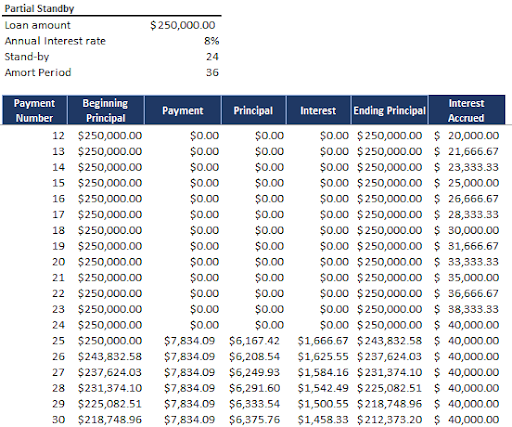

Putting a Note on Stand-by

Lastly, an important financing structure to discuss is standby financing. A standby seller financing option is either considered to be put on “partial stand-by" or “full stand-by". A standby financing structure is typically pursued for firms that are having a difficult time gaining SBA loan approval. For a partial standby financing structure, what happens is that the buyer (borrower) is not expected to make monthly payments at all until the financing contract states that payments must be made. The structure allows the buyer to borrow for a specified period of time without having to make payments (principal or interest). Below is an example of partial standby financing:

Detailed in the above example, the partial standby financing structure states that the buyer doesn’t have to make payments until 2 years into the contract. At that point, there is only 3 years remaining on the loan, so the calculated payment will act the same way as a straight payment loan.

It’s important to note that as a buyer, some structures may offer better terms for a specific business compared to another. Or some loans may have a lower interest rate altogether, particularly when a seller wants a specific type of financing.

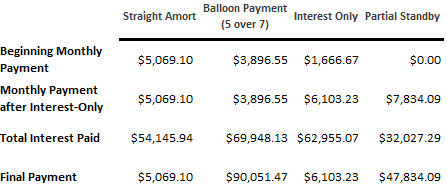

Summary Table of Different Structures in Seller Financing

Below is a summary of the most common types of seller financing structures and how they compare to a straight payment structure.

Note that for the above loans that each of them have a term limit of 5 years (i.e., 60 monthly payments). Notice that the monthly payment determines the amount of interest a buyer will pay for the entire duration of the contract.

Negotiating Seller Financing 101:

Pursuing seller financing is similar to pursuing a conventional bank loan from a lender. First and foremost, a buyer must understand the seller’s concerns and make sure there are constraints (covenants) built into the financing that would elevate the seller’s concerns. After all, the seller is more than likely funding the majority of the purchase price, so the seller is viewing the transaction as an investment.

Moreover, it is imperative that buyer’s build a relationship with the seller. One, building a relationship builds trust between the buyer and seller, but two, it allows for tough conversations to be had throughout the financing timeline..

As a buyer, articulating the benefits of seller financing to the seller is crucial. For example, upfront costs are significantly less than if the transaction is done through a lender. In addition, the seller is able to sell its business faster than going through a lender or some other third party vendor. Moreover, the buyer needs to explain the needs from financing partners.

Clearly there are benefits and drawbacks to seller financing; however, it is important to note that one type of financing is not right for every deal or deal structure. There are many variables (industry, stage of the company, buyer’s net worth, buyer’s experience, etc.) that will make certain financing more favorable compared to others.

Information posted on this page is not intended to be, and should not be construed as tax, legal, investment or accounting advice. You should consult your own tax, legal, investment and accounting advisors before engaging in any transaction.

Get the latest in your inbox

Join our bi-weekly SMB newsletter. It's free and not annoying.

This website (the “Website”) is owned and operated by Mainshares, LLC (“Mainshares”). By accessing the Website and any pages thereof, you agree to be bound by Mainshares’ Terms of Service and Privacy Policy, as well as the Terms of Service and Privacy Policy for Main Street Securities, LLC (“Main Street”). The information contained herein is provided for informational purposes only and is not intended to influence any investment decision or be a recommendation for any investment, service, product, or other advice of any kind, and shall not constitute or imply an offer of any kind. The products and services offered by Mainshares are not offered by a certified public accountant (“CPA”) and should not be considered as a substitute for services provided by a CPA.

The information contained herein is provided by Mainshares, LLC (“Mainshares”) for informational purposes only and is not intended to influence any investment decision or be a recommendation for any investment, service, product, or other advice of any kind, and shall not constitute or imply an offer of any kind. The products and services offered by Mainshares are not offered by a certified public accountant (“CPA”) and should not be considered as a substitute for services provided by a CPA.

Broker-dealer services provided in connection with some of the investment opportunities on the Mainshares platform are offered through Main Street, a registered broker-dealer, affiliate of Mainshares, and member of FINRA/SIPC. For additional information, please contact your licensed securities representative of Main Street Securities LLC or visit FINRA’s BrokerCheck. If the investment opportunity does not include the "Brokered by Main Street Securities" designation, broker-dealer services were not provided in connection with the offering through Main Street.

Neither Mainshares nor Main Street Securities LLC make investment recommendations and no communication, through this Website or in any other medium should be construed as a recommendation for any security offered.

Should you be presented with an investment opportunity, such investment opportunities involve private, unregistered securities that are speculative and involve substantial risk. These investment opportunities are conducted in accordance with an exemption from registration, specifically relying on the private offering provision outlined in Section 4(a)(2) of the Securities Act of 1933, along with compliance with Rule 506 of Regulation D. All investments involve risk and the past performance of a security, or financial product does not guarantee future results or returns. There is always potential to lose money when you invest in securities or other financial products. Private placements lack liquidity and distributions are not guaranteed. You are strongly encouraged to seek professional advice prior to entering into any transaction for any securities and to consider your investment objectives and risks carefully before investing.

Neither the SEC nor any federal or state securities commission or regulatory authority has recommended or approved any investment or the accuracy or completeness of any of the information or materials provided herein or through any references/links herein. There can be no assurance that any valuations provided by issuers are accurate or in agreement with market or industry valuations. Neither Mainshares nor Main Street Securities LLC make any representations or warranties as to the accuracy of such information.