Hong Kong welcomed its new open-ended fund company (OFC) corporate structure on 30 July 2018, following 4 years of market consultation and legislation. The introduction of the OFC brings further flexibility to fund managers seeking to establish a Hong Kong domiciled investment vehicle, and is a welcome alternative to the existing unit trust structure currently available for Hong Kong domiciled funds in Hong Kong’s $18 trillion fund management industry. The OFC strikes an attractive balance for investors and fund managers alike between providing investor protection and familiarity of a company limited by shares with the simplicity of fund raising previously only available for unit trusts in Hong Kong.

The arrival of the OFC provides Hong Kong with a corporate structure comparable to the UK’s Open-Ended Investment Company (OEIC), Luxembourg’s Société d'Investissement à Capital Variable (SICAV), Singapore’s upcoming Singapore Variable Capital Company (S-VACC) and Australia’s forthcoming Collective Corporate Investment Vehicle (CCIV). It remains to be seen whether fund managers will be enticed to establish OFCs in Hong Kong. For private fund managers currently setting up private funds in offshore jurisdiction such as the Cayman Islands, the most notable advantage of an OFC over a Cayman vehicle lies in the simplicity of dealing with a single jurisdiction if those fund managers already operate in Hong Kong, although this is balanced against being subject to a light touch regulatory oversight by the Securities and Futures Commission of Hong Kong (SFC) and potential Hong Kong tax considerations. A Hong Kong domiciled OFC also offers the benefit of potentially enabling fund managers to participate in the Mainland-Hong Kong Mutual Recognition of Funds Scheme, allowing publicly offered OFCs to be distributed to Mainland investors.

OFCs at a glance

An OFC:

|

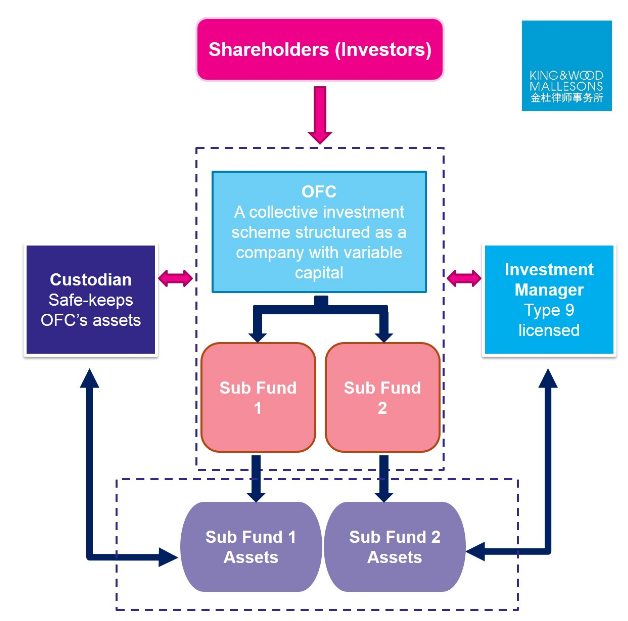

OFC structure

An OFC’s board of directors (comprising at least 2 individuals, one being independent of the custodian) must delegate all responsibilities for management of the OFC, including in respect of valuation and pricing of fund assets, to a third party investment manager who is licensed or registered for Type 9 regulated activity by the SFC.

An OFC must also appoint a custodian to segregate its assets from those of the investment manager. The custodian’s duties are comparable to those currently applicable to custodians in respect of unit trusts under the SFC’s Code on Unit Trusts and Mutual Funds (UT Code). The custodian should meet the same eligibility requirements which are applicable to SFC authorised funds under the UT Code.

Umbrella funds

Similar to the Hong Kong unit trust structure, an OFC may be established as an umbrella structure with several operationally distinct sub-funds, each with its own investment objectives. Statutory segregation of sub-funds’ assets and liabilities ensures the sanctity of other sub-funds is not breached in the event of a sub-fund’s insolvency, adding to the umbrella structure’s appeal. Each sub-fund may also create multiple share classes.

SFC approval

The SFC has issued a Code on Open-Ended Fund Companies (OFC Code), which sets out the requirements for establishing an OFC, as well as the ongoing compliance obligations for an OFC. These requirements include:

- applying to the SFC for registration and approval by the SFC;

- filing of the offering document of the OFC with the SFC;

- post-registration filings to the SFC of certain material changes to the OFC; and

- preparation of audited annual reports.

In the case of private OFCs, at least 90% of fund assets will be required to be invested in securities, cash, bank deposits, certificates of deposit, foreign exchange contracts and foreign currencies.

Publicly-offered OFCs, which are subject to the UT Code, will continue to be subject to the same level of regulatory oversight by the SFC. However, private fund managers may consider the OFC regulatory requirements to be comparatively more onerous than offshore fund structures in other jurisdictions such as the Cayman Islands.

Tax treatment

Publicly-offered OFCs continue to enjoy profits tax exemption as all SFC authorised collective investment schemes do. A privately offered OFC may also qualify for a profits tax exemption if it can fulfil certain qualifying requirements. For example, a private OFC must demonstrate that it is not closely held by a limited number of investors (at least 5 or 10 investors, depending on the type of investors an OFC has), and that the OFC only carries out qualifying transactions[1].

What’s next? Get prepared!

Fund managers should start talking to their professional advisors, custodians and investors to consider the potential opportunities in this new regime.